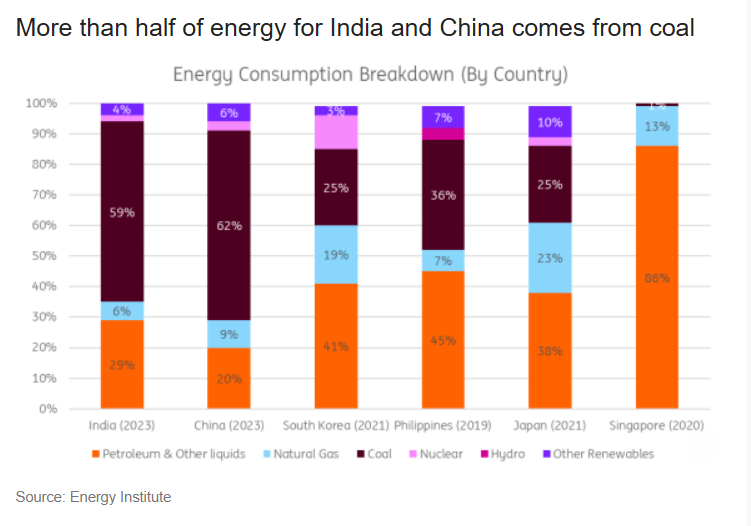

India and China are likely to be less exposed to oil shocks because coal still provides more than half of their energy requirements.

A central concern for policymakers currently revolves around the timeline for rising oil prices to significantly impact Asian economies.

The conflict between the US and Israel, with Iran has led to an agonising blockade in the Strait of Hormuz.

The blockade has pushed oil and gas prices to multi-year highs as supplies continue to remain disrupted.

“Under a scenario where supply disruptions last for a month and then gradually ease throughout the year, we expect Brent crude oil to average US$83/bbl, about $15/bbl higher than the 2025 baseline,” Deepali Bhargava, regional head of research, Asia Pacific at ING Group, said in a report.

Energy adequacy varied across Asia

Based on ING’s prior analysis of import exposures, Thailand and Korea face the highest risk from oil and gas supply shocks and price increases in Asia due to their substantial trade deficits in these commodities.

Taiwan, the Philippines, Singapore, and India also face notable, though diverse, vulnerabilities.

The extent of these vulnerabilities is shaped by domestic buffers and specific pricing policies in each country.

Energy reserve adequacy is highly varied across Asia.

Japan boasts the most substantial cushion, with reserves sufficient for 254 days of domestic demand.

South Korea follows with reserves covering 210 days.

In contrast, India’s reserves stand at approximately 74 days.

“While oil inventories appear broadly sufficient in the near term, LPG buffers remain notably thin, increasing vulnerability to price spikes and supply disruptions,” Bhargava said.

The 70% surge in LNG prices following the conflict has disproportionately affected economies heavily dependent on imported gas—specifically Thailand, India, Korea, and Japan—leaving them highly vulnerable to ongoing price instability.

Coal dependence helps India and China

The extent of fuel substitution serves as a crucial distinction across the region.

India and China possess an inherent shock absorber, given that coal still accounts for over half of their energy supply.

“Although both remain net coal importers, their ability to substitute oil with coal at the margin provides an important cost advantage,” Bhargava said in the report.

Natural gas prices have surged by approximately 70% since the conflict started, creating a stark contrast with the much more modest 12% rise seen in coal prices over the same period, according to ING.

“This divergence gives India and China a meaningful substitution buffer that could reduce their exposure to oil and gas price spikes to some extent,” Bhargava added.

Market impact

Singapore, Korea, and Taiwan are better positioned to absorb rising import costs due to their substantial current account surpluses, which act as a significant buffer.

In contrast, Thailand’s current account surplus is considerably smaller, providing less protection against these higher costs.

India and the Philippines are unique among major economies in maintaining structural current account deficits; however, New Delhi has successfully limited its deficit to approximately 1% of GDP in recent years.

The risk profile is further complicated by foreign exchange (FX) reserve adequacy, according to Bhargave.

Specifically, Malaysia, Indonesia, and South Korea possess relatively lower FX cover compared to their import requirements, which increases their vulnerability to a sustained increase in crude oil prices.

With robust FX buffers, the Philippines and India have enhanced capacity to address currency pressures should oil-related outflows increase, a contrast to other nations, Bhargava said.

For the time being, oil price risks appear manageable because oil marketing companies are currently absorbing the rising crude costs instead of passing them on to retail prices, according to her.

“As a result, we are keeping our CPI inflation forecast unchanged and continue to expect inflation to average below the RBI’s medium‑term target of 4% in 2026.”

However, the INR’s vulnerability persists, as increased crude prices are expected to broaden the current account deficit, thus placing further strain on the currency, Bhargava noted.

The post India, China less exposed to oil shocks for now; coal dependence key buffer appeared first on Invezz